It’s been an especially challenging year for small-cap value investors.

Last quarter, we discussed risk-taking returning to the marketplace, led by a frenzy in artificial intelligence and mega-cap technology stocks. As the Federal Reserve continued to raise interest rates, offering 5.5% on short-term Treasuries, it was difficult to comprehend the lofty multiples being paid for a very narrow group of “growth on the come” businesses. To some extent, the air has been let out of this last balloon. But in our view, more is in store for overvalued, over-owned growth and momentum favorites.

Our portfolio experienced a modest level of activity during the period, adding four new positions. It’s not that we aren’t actively looking for opportunities—we are. But as the legendary hedge fund manager Seth Klarman pointed out, value investing “requires deep reservoirs of patience and discipline.”

As contrarians, we look for prospects not in what the herd is buying but what it’s selling or ignoring. Going against the crowd can be difficult because it requires a willingness to be “initially wrong” for extended stretches, Klarman noted, until rational thinking returns to the market. It also demands fortitude to wait until investments trade at prices that are truly attractive relative to their intrinsic value. That’s how we have always invested—and what we’re especially focused on today.

To be sure, we are underexposed to higher-beta, early-cycle stocks. This is not a top-down call. Rather, it’s a reflection of the fact that many names on our watchlist aren’t at or near potential entry points. We’re willing to take pitches—as many as we have to—until hanging curve balls start coming over the plate. We will only swing when companies with attractive risk/reward characteristics fit our 10 Principles of Value Investing™.

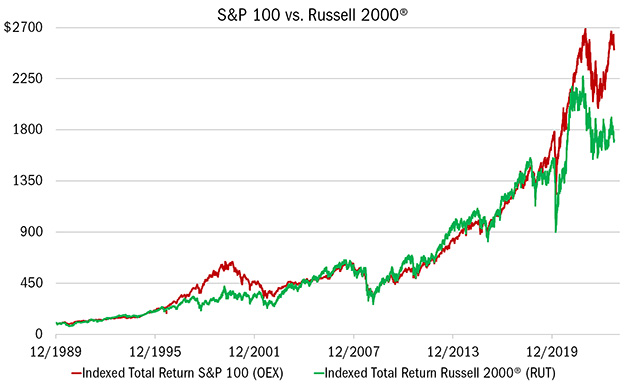

We wouldn’t be surprised to start spotting more of those opportunities soon. Part of that is seen in how poorly small caps have been doing, compared to the largest stocks, as measured by the S&P 100 Index (see chart below). The relative outperformance of large caps, led by the so-called Magnificent 7, is disconcerting and suggests more volatility to come as the long lags of Federal Reserve interest rate hikes gradually work their way into the broader economy and markets.

Historically, excessive gains by a narrow group of companies—in this case, the mega caps—has led to a significant correction in the opposite direction. To us, this disparity will be corrected and is a sign to remain patient and disciplined in the months and quarters ahead.

Source: FactSet; FTSE Russell, Daily data 12/29/1989 to 9/29/2023. The data in this chart represents a $100 investment in the S&P 100 (OEX) compared to the Russell 2000® (RUT) on a total return basis, which tracks both the capital gains as well as cash distributions (such as dividends, interest, and other realized distributions) attributed to the respective Index. Past performance does not guarantee future results. There is no guarantee that a particular investment strategy will be successful.

The markets are presently operating under two related assumptions. First, there’s the notion that the Federal Reserve has largely won the war against inflation after raising rates 11 times since March 2022. Given the unprecedented flood of stimulus during and after the pandemic, we’re not convinced this is true—at least not yet. Second, as banks continue to tighten lending standards while consumer loan delinquencies are climbing, the “soft landing” that many investors now expect is up for debate.

As those economic expectations are tested in the coming months, we wouldn’t be surprised to see more handwringing in the markets, along with opportunities.

Attribution Analysis & Portfolio Activity

For the quarter, the Heartland Value Fund outperformed the Russell 2000® Value Index, with a return of -1.02% versus -2.96% for the benchmark. In a difficult market, the Fund generated gains in Energy (+22.21), Utilities (+5.59%), and Financials (+2.71%), owing largely to stock selection.

Throughout the year, we’ve done a decent job of taking what the market gives us, both on the upside (selling or paring down positions as they’ve hit target prices) and downside (buying beaten-down names once they fall to the right price).

Below are examples of that selectivity:

Consumer Discretionary. Mohawk (MHK), the leading manufacturer of flooring products such as carpet, tile, wood, and vinyl products for the residential and commercial markets, ran into stiff headwinds in recent years as inflation increased costs on source materials. This compressed MHK’s margins, and the stock price was nearly cut in half between June 2021 and early this year. We believe the worst of those pricing pressures are behind the business, which stands to benefit from the ongoing growth in home remodeling and office space conversions as the commercial real estate market struggles with hybrid work.

After initiating a position in Mohawk this Spring, we added to it during the quarter as the market sold off. While it’s not ideal that MHK continued to fall, the slide has allowed us to build an over 2% allocation in a name our research indicates is a long-term alpha generator at a compelling valuation.

Mohawk is priced at half of sales, less than tangible book value, and 9X our estimate of ‘23 earnings. With ample free cash flow and active share buybacks, we believe MHK possesses favorable risk-reward characteristics.

Utilities. National Fuel Gas (NFG) is another existing holding we added to in the quarter. NFG is an energy company, with regulated utility assets, involved in the production, transportation, and distribution of natural gas. The stock’s correlation with natural gas prices has been high, so it wasn’t too surprising when the stock fell as natural gas prices declined following last year’s benign winter.

But prices are expected to rebound in the coming months now that the supply issue has been addressed with the steep drop in oil gas rig counts. Demand is also set to improve starting in 2025 with the onset of more U.S. liquefied natural gas (LNG) exports. Meanwhile, this is a well-run business with a track record of financial soundness. NFG, for instance, has raised dividends for 53 consecutive years because of the consistent cash flow generation from its midstream and utility segments.

Yet, when looking at valuations, we see a disconnect. NFG is trading at a 20% discount to its historical valuations compared with traditional oil and gas exploration and production stocks. The relative premium it typically garners is a function of the company’s ability to leverage its pipeline infrastructure to capitalize on higher natural gas prices and the stability of non-energy cash flows. We are positioning the portfolio to take advantage of this opportunity.

Financials. With a 10% market share, Stewart Information Services (STC) is the smallest of the four companies enjoying an oligopoly in the title insurance industry.

While most people don’t think about title insurance when purchasing a home, policies indemnify homeowners and lenders against title defects that could result in significant loss arising from back taxes, liens, and other claims. Ever since a proposed sale to larger peer Fidelity National Financial was blocked by the Federal Trade Commission in 2019, STC has been in need of a new direction. Since being named CEO that same year, Fred Eppinger has set out to improve the company’s margin structure and take market share.

These operational improvements, however, have been hidden by lower top-line volume as rising mortgage rates have curtailed home transactions. As a result, STC shares fell to nearly 90% of book value, well below its 10-year average of 1.3X.

As housing sales normalize over time and revenues recover, we view STC’s earnings to have significant upside and the stock should trade closer to its historic average. Moreover, the realization of its improved margin structure could result in a multiple that’s closer to peers First American Financial and Fidelity National Financial, which have historically traded at a premium to STC.

Outlook

While waiting for those hanging curve balls, we are sticking to our process. Guided by the 10 Principles of Value Investing™, we are laser-focused on identifying well-managed, financially strong companies with resilient balance sheets that offer compelling valuations. We feel good about the opportunities ahead but are content to keep our powder dry if entry points don’t materialize. As Seth Klarman advised, value investing requires deep reservoirs of patience and discipline.

Fundamentally Yours, The Heartland Team