We’ve been monitoring Amazon.com Inc (AMZN) for several years because valuations have become more attractive as the business matures. Until now, Amazon has traded at a meaningful premium to the S&P 500 Index and peers including large retailers and cloud-computing competitors.

The company tends to invest capital in massive waves creating significant earnings noise. For example, they doubled their retail distribution center footprint in just over a year following the COVID-19 pandemic, causing the company’s free cash flow and profit margins to drop. However, the areas they’re investing in, such as Amazon Web Services (AWS), advertising, and subscriptions are higher-margin businesses, which should lead to better long-term profitability.

Right now, Amazon is spending big on artificial intelligence (AI) infrastructure. This investment will likely make profits look weaker in the short term, but it should help Amazon two ways:

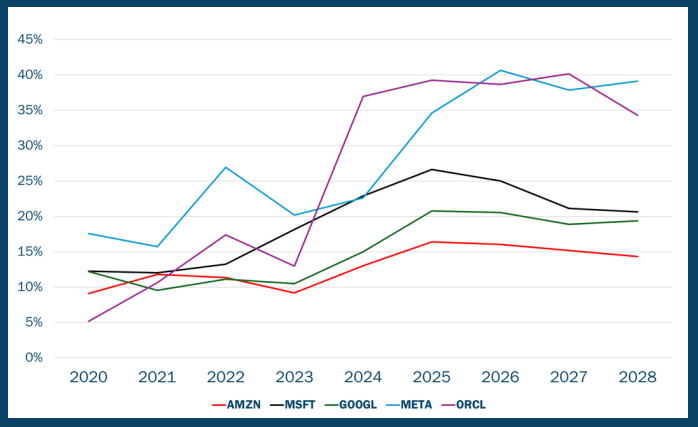

Despite skepticism around its AI positioning, AWS seems to be well-placed to benefit from AI trends, and Amazon has surprisingly become relatively efficient with its capital investments. Historically, Amazon was rightfully seen as a more capital-intensive business than large-tech competitors including Alphabet (Google), Microsoft, Oracle, and Meta (Facebook). Today, Amazon is the most capital efficient operator as measured by capital expenditures relative to sales.

Sourse: FactSet Research Systems, Inc. Annual Data from 2020-2028. The data in the chart represents the capital expenditures to sales ratio for Amazon.com, Inc. (AMZN), Microsoft Corporation (MSFT), Alphabet, Inc. (GOOGL), Meta Platforms Inc. (META) and Oracle Corp (ORCL). Capital expenditures (CapEx) are the funds companies allocate to acquire, upgrade, and maintain essential physical assets like property, technology, or equipment, crucial for expanding operational capacity and securing long-term economic benefits. Past performance does not guarantee future results. Periods after 6/30/25 are estimated.

The market is rewarding AI-related capex growth at other companies where the payback is shorter. For example, Oracle, has increased capex so much that we don’t expect any free cash flow generation for several years. Oracle datacenters are being used to trail AI models today, but the long-term viability of this business model could be called into question as model training moderates.

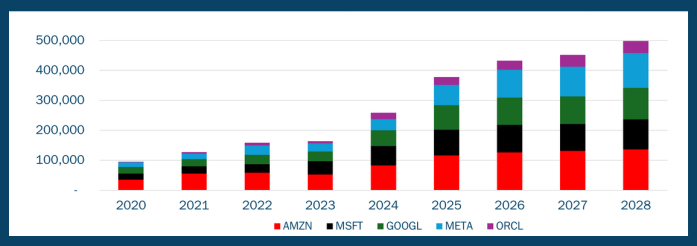

FactSet Research Systems Inc. Annual Data from 2020-2028. The data in this chart represents the Capital expenditures predictions for AMZN, MSFT, GOOGL, META, & ORCL overtime. Past performance does not guarantee future results. Periods after 6/30/25 are estimated.

When considering the value of its high-margin businesses like AWS and ads, Amazon appears to be relatively undervalued on a historical basis. Based on our research and evaluation, we believe we are getting its dominant e-commerce business for free. This dynamic provides us with a margin of safety, and the retail business provides significant free cash flow that can be utilized for greater investments. Most businesses require capital to grow, but Amazon’s retail business operates with negative working capital meaning Amazon gets paid before they pay suppliers. As a result, the faster retail grows, the more cash there is available for attractive long-term investments.

©2026 Heartland Advisors | 790 N. Water Street, Suite 1200, Milwaukee, WI 53202 | Business Office: 414-347-7777 | Financial Professionals: 888-505-5180 | Individual Investors: 800-432-7856

Past performance does not guarantee future results.

Investing involves risk, including the potential loss of principal.

Statements regarding securities are not recommendations to buy or sell.

There is no guarantee that a particular investment strategy will be successful.

Value investments are subject to the risk that their intrinsic value may not be recognized by the broad market.

The statements and opinions expressed in the articles or appearances are those of the presenter. Any discussion of investments and investment strategies represents the presenters' views as of the date created and are subject to change without notice. The opinions expressed are for general information only and are not intended to provide specific advice or recommendations for any individual. Any forecasts may not prove to be true.

Economic predictions are based on estimates and are subject to change.

CFA® is a registered trademark owned by the CFA Institute.

As of 8/19/2025, Heartland Advisors on behalf of its clients held less than 1% of the total shares outstanding of Alphabet, Inc. (GOOGL) and Amazon.com, Inc. (AMZN). Statements regarding securities are not recommendations to buy or sell. Portfolio holdings are subject to change. Current and future holdings are subject to risk. Microsoft Corporation (MSFT), Meta Platforms Inc. (META) and Oracle Corp (ORCL) are unowned by Heartland Advisors, Inc.

Heartland’s investing glossary provides definitions for several terms used on this page.