As active managers, we know how difficult it is to predict the direction of the market. With so many uncontrollable factors, we try to focus on the things that we can influence, such as our assessment of the fundamentals and vulnerabilities of the securities we’re considering. This involves constantly reviewing our own processes and performance, to find areas where we can improve. Devotion to constant, never-ending improvement is core to everything we do here at Heartland.

In that vein, we’ve decided to revisit some of the forecasts we’ve made as part of this video series over the past year, to see what lessons we can learn.

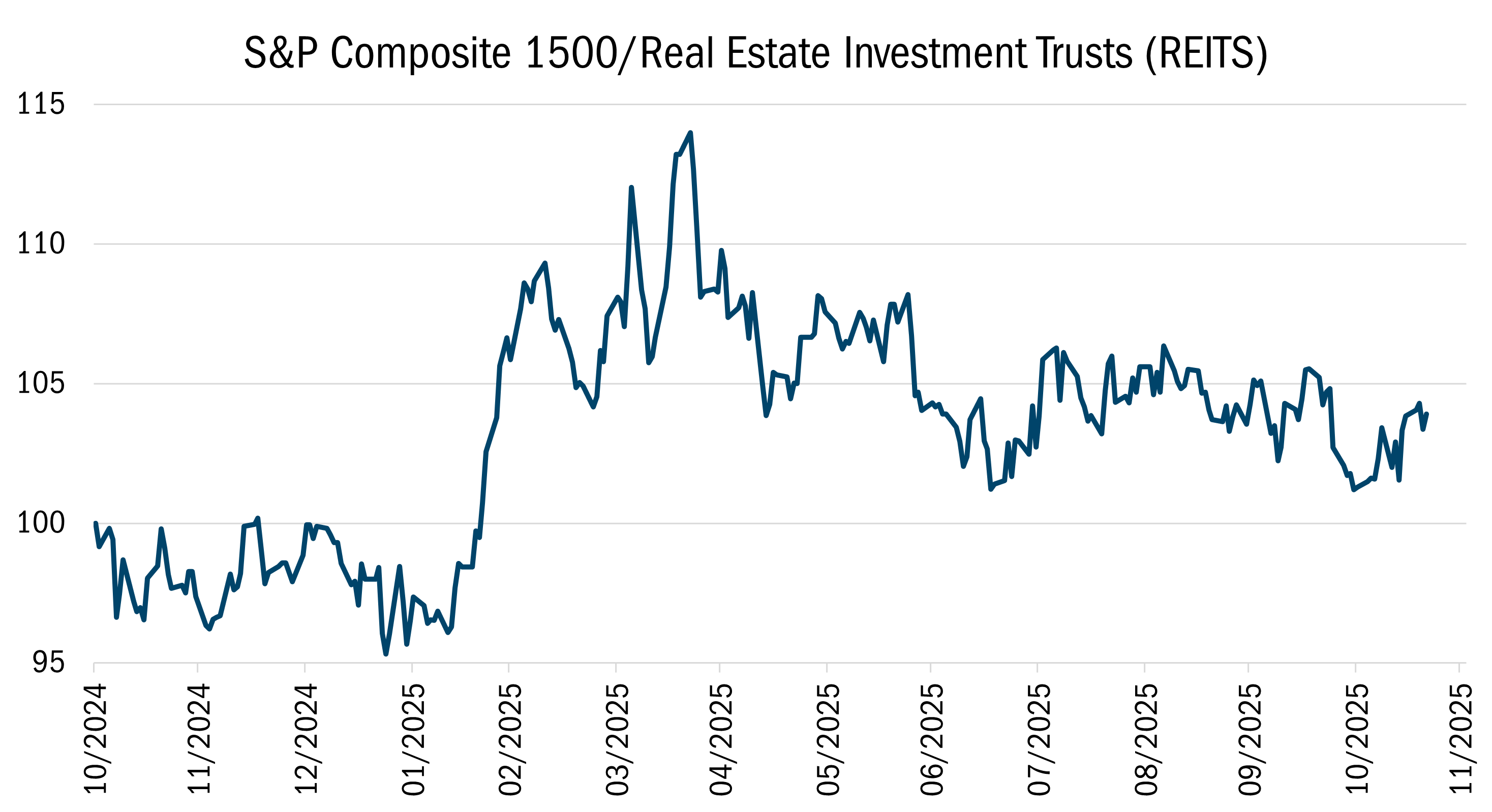

Last November, we discussed our perspective on the real estate sector, especially after many real estate investment trusts (REITs) significantly lagged the market for the past three years. As value managers who believe in reversion to the mean and understand the return potential of stocks trading below their intrinsic value, identifying overlooked or beaten down parts of the market is part of our DNA.

Were we right with REITs? Yes and no. Yes, this group has slightly outperformed over the past year, but not nearly as much we had hoped. Still, we note that REIT outperformance has historically taken place in long rallies in between multi-year periods of underperformance. So, the jury is still out on that call.

Source: FactSet Research Systems Inc. Daily data 10/31/2024 to 11/20/2025. The data in this chart represents the S&P Composite 1500 compared to the Real Estate Investment Trusts. All indices are unmanaged. It is not possible to invest in an index. Past performance does not guarantee future results.

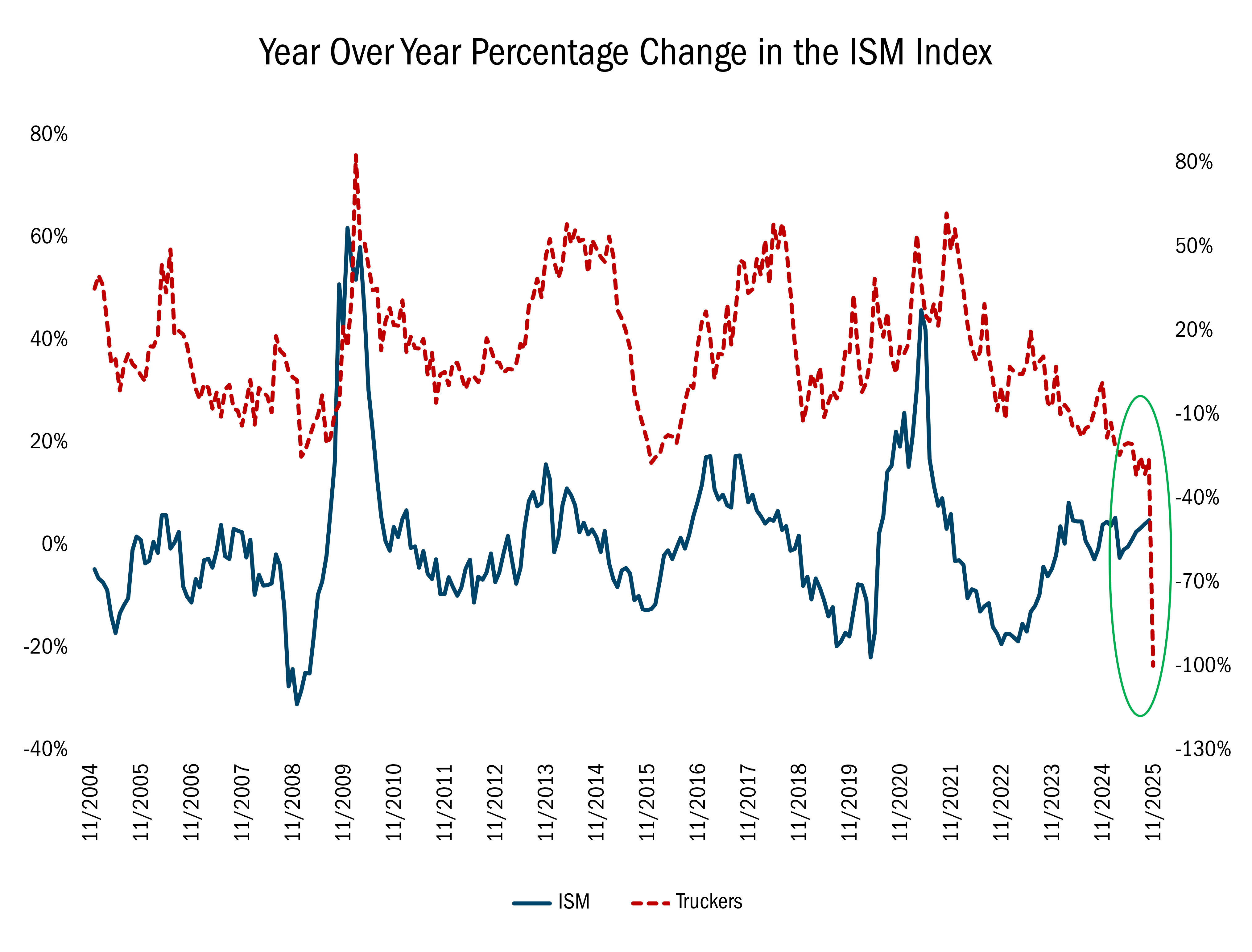

At the end of 2024, we also predicted that the trucking industry could be the canary in the coalmine for the economy. At the end of last year, there were many reasons to be hopeful for economic expansion, including anticipation of Federal Reserve interest rate cuts. That easing cycle, however, didn’t begin until September 2025 as inflation concerns lingered throughout the year. There were many other factors affecting the manufacturing sector, including uncertainties surrounding federal trade policy and tariffs. The result: The ISM Manufacturing PMI Index continued to weaken throughout the year, as did most trucking stocks.

Source: FactSet Research Systems Inc. Daily data 11/31/2004 to 11/20/2025. The data in this chart represents the Year over Year percentage change in the ISM index. ISM Manufacturing Index is based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production inventories, new orders and supplier deliveries. A composite diffusion index is created that monitors conditions in national manufacturing based on the data from these surveys. All indices are unmanaged. It is not possible to invest in an index. Past performance does not guarantee future results.

This reinforces why we believe in bottom-up stock picking. While macro views of the economy and policy can certainly help inform our thinking, decisions to initiate a new holding in our portfolio or remove an existing security are driven by fundamental analysis of the underlying business where we have more control.

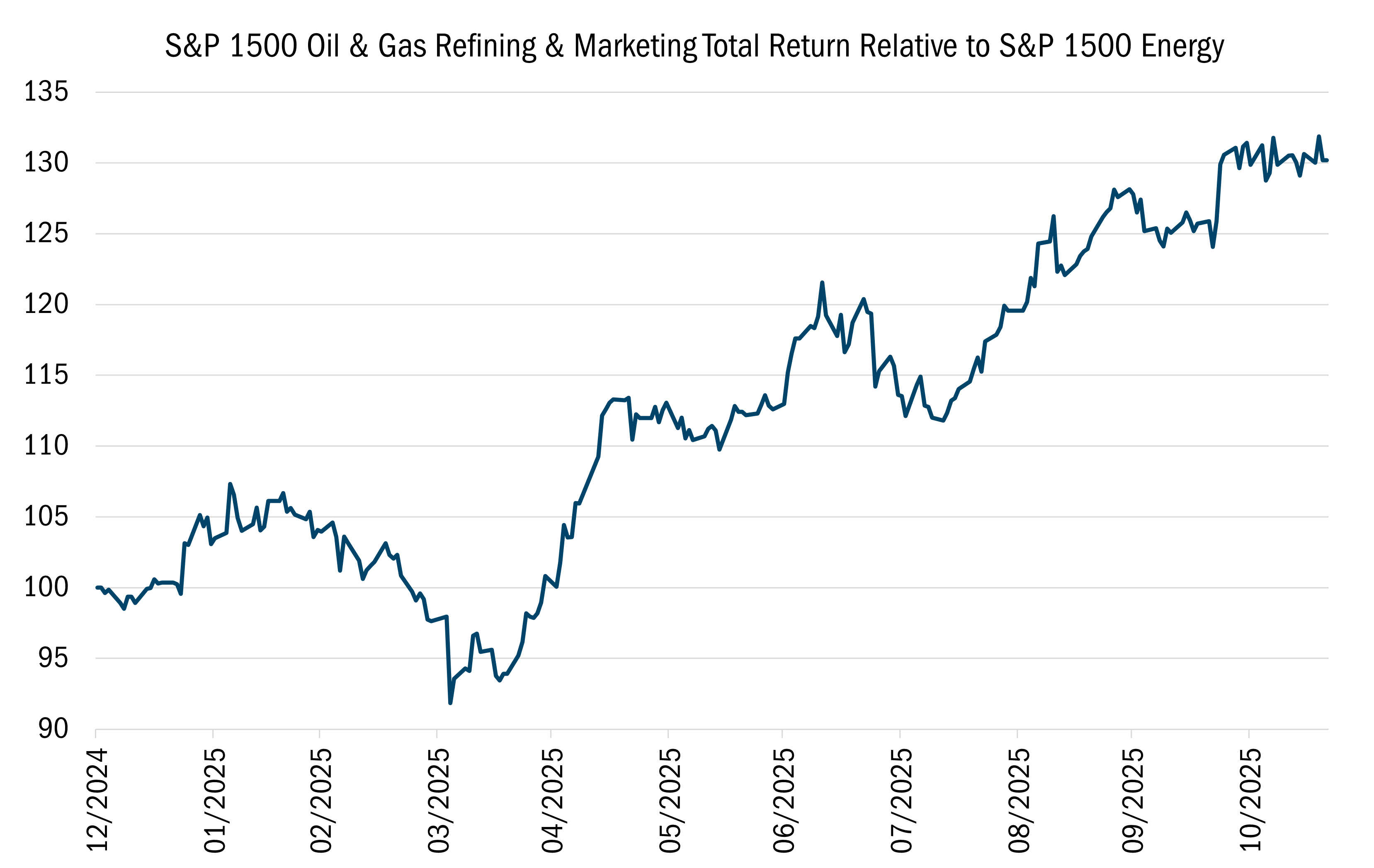

In January, we looked at another economically sensitive sector: U.S. oil refiners. Expectations of an economic rebound also played into the case for the energy sector, as did expectations that the Trump administration would advocate for friendlier policies for fossil fuel production. But another reason we were particularly drawn to refining stocks was the increase in insider buying, suggesting that either valuations were growing attractive, or fundamentals were about to improve, or both. Ultimately, we saw oil production pick up and refining stocks have been outpacing the broader energy sector.

FactSet Research Systems Inc. Daily data 12/31/2004 to 11/20/2025. The data in this chart represents the S&P 1500 Oil & Gas Refining & Marketing Total Return Relative to S&P 1500 Energy. All indices are unmanaged. It is not possible to invest in an index. Past performance does not guarantee future results.

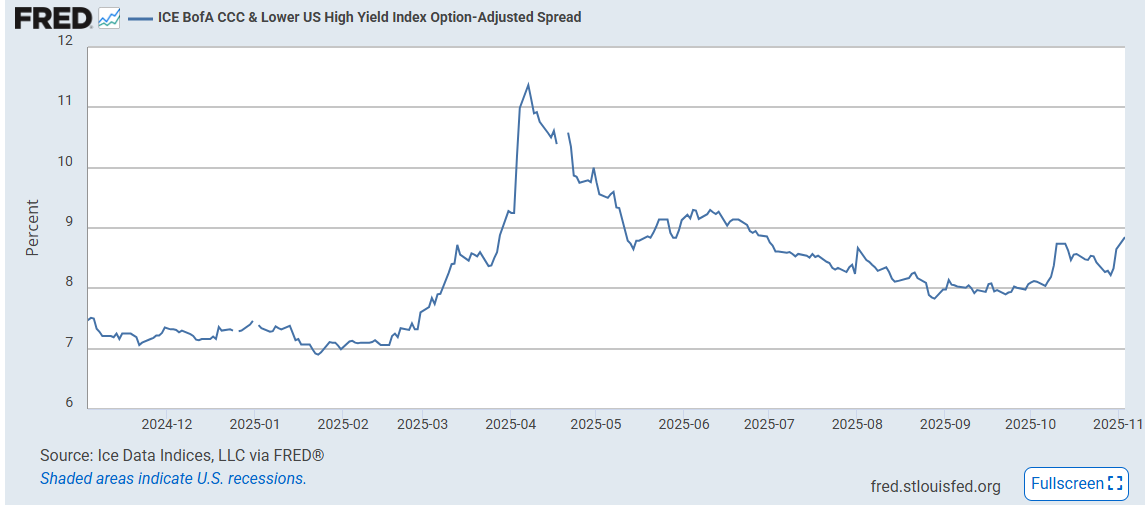

In February, we touched on the credit markets and suggested that credit spreads, particularly for high yield debt, were unusually tight. Given that there were a lot of uncertainties surrounding the economy, we thought credit spreads would revert to the mean and widen. That, in fact, has been the case.

Source: Ice Data Indices, LLC via FRED. Monthly data 12/31/2024 to 11/20/2025. The data in this chart represents displays the ICE BofA CCC & Lower U.S. High Yield Index Option-Adjusted Spread, which measures the additional yield investors require to hold CCC-rated and below U.S. corporate bonds compared with U.S. Treasuries. All indices are unmanaged. It is not possible to invest in an index. Past performance does not guarantee future results.

In March, we talked about the importance of free cash flow, which is part of our 10 Principles of Value Investing™. Free cash flow, which represents the cash that a business has available for discretionary initiatives after operating expenses and capital expenditures, is particularly important because it allows companies to create their own destiny through share buybacks, dividend payouts, or mergers and acquisitions. But we’re mindful that there are periods when factors such as free cash flow and profitability are overshadowed by massive speculation.

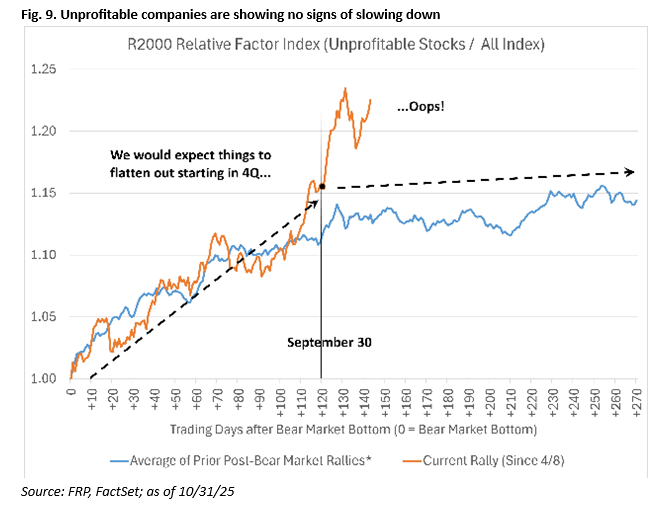

We appear to be in a heavily speculative environment. Since the market hit its April lows associated with the White House’s “Liberation Day” announcement of tariffs, the Russell 2000 Value Index is up a little over 30%. The speculative nature of the current market is emphasized by the fact that companies with no sales are up more than 150%. Conventional wisdom says that as the market broadens out, quality factors should catch up. But that hasn’t taken place thus far. As the chart below shows, the advantage that unprofitable stocks in the Russell 2000® Index have relative to the broader benchmark has not slowed down thus far this quarter.

Source: Fuery Research Partners and FactSet. Daily data from 4/8/25 to 10/31/25 (for Current Rally)The data in this chart Compares the relative performance of Unprofitable Russell 2000 stocks in the bull market started on 4/8 to that of their performance at the start of prior bull markets. All indices are unmanaged. It is not possible to invest in an index. Past performance does not guarantee future results.

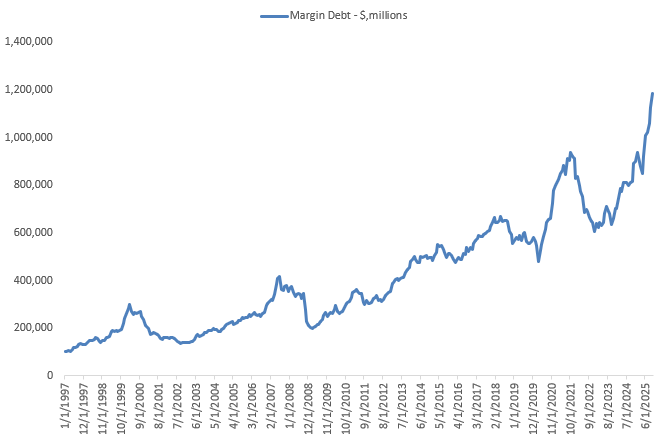

It's not uncommon to see low-quality businesses outperform in the early stages of a bull market, but the scope and severity of the rally among non-earners and businesses with no sales has been off the charts. Other factors, such as growing margin debt, further highlights the speculation that is growing around AI-related companies.

Source: FINRA. Data as of 9/30/2024 – 10/31/2025. The data in this chart shows the historical level of U.S. margin debt, illustrating how borrowing against investment portfolios has evolved over time. The data highlights long-term growth in margin debt with notable peaks during periods of heightened market activity. All indices are unmanaged. It is not possible to invest in an index. Past performance does not guarantee future results.

While this isn’t surprising, we think investors might be missing out on some great undiscovered opportunities beyond this narrow patch of the market. We believe that a reversion to mean is likely, where lower-quality businesses begin to lag those that have better fundamentals associated with key considerations such as profitability or return on capital.

We understand that fundamental factors such as return on capital or free cash flow may not seem as compelling as AI. But, if the past 40 years have taught us anything, it’s that bottoms-up fundamentals drive performance over the long run. Yet even a long track record does not eliminate the need for improvement.

This past year of reflection has reminded us that markets, like all complex systems, evolve. When assumptions fail or when conditions shift, the opportunity lies not in defending past beliefs, but in examining mistakes and improving the process. This willingness to learn from past decisions is imperative to overall development.

Continuous improvement, driven by curiosity, acknowledgment, and a solid investment process, becomes both a discipline and a competitive advantage, laying the foundation for success in 2026 and beyond.

©2026 Heartland Advisors | 790 N. Water Street, Suite 1200, Milwaukee, WI 53202 | Business Office: 414-347-7777 | Financial Professionals: 888-505-5180 | Individual Investors: 800-432-7856

Past performance does not guarantee future results.

Investing involves risk, including the potential loss of principal.

There is no guarantee that a particular investment strategy will be successful.

Value investments are subject to the risk that their intrinsic value may not be recognized by the broad market.

Sector and Industry classifications are sourced from GICS®.The Global Industry Classification Standard (GICS®) is the exclusive intellectual property of MSCI Inc. (MSCI) and S&P Global Market Intelligence (“S&P”). Neither MSCI, S&P, their affiliates, nor any of their third party providers (“GICS Parties”) makes any representations or warranties, express or implied, with respect to GICS or the results to be obtained by the use thereof, and expressly disclaim all warranties, including warranties of accuracy, completeness, merchantability and fitness for a particular purpose. The GICS Parties shall not have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of such damages.

Economic predictions are based on estimates and are subject to change.

Heartland Advisors’ 10 Principles of Value Investing™ consist of the following criteria for selecting securities: (1) catalyst for recognition; (2) low price in relation to earnings; (3) low price in relation to cash flow; (4) low price in relation to book value; (5) financial soundness; (6) positive earnings dynamics; (7) sound business strategy; (8) capable management and insider ownership; (9) value of company; and (10) positive technical analysis.

Heartland’s investing glossary provides definitions for several terms used on this page.